1/30/2008

Affiliations

|

|

3/30/2009 --- Continue Reading This Post ---

Buying The Presidency

Republican Presidential Candidate Mike Huckabee spoke about campaign finances the other day, and his comments struck me as being very interesting.

It's also raging in paid advertising on TV and radio. Romney has spent $30 million on TV ads in Florida this year. That's five times as much as the McCain campaign, which is now using less-expensive radio commercials to directly question Romney's credibility on the economy.

So how's that working out for you, Mitt?

--- Continue Reading This Post ---

- He spoke about operating his campaign in the black and not borrowing money to finance it.

- He also mentioned that he was not in a position to cut a big fat check from his personal fortune to keep his campaign afloat.

And back to Mittens... Is this the same man who a year ago told reporters that it would be "akin to a nightmare" for him to have to spend his own money on his campaign, rather than, ya know, relying on voter support in the form of donations? Indeed it is. In fact, at the time of his comment, he had already dropped a couple mil of his own money. And this makes you an economic leader as seems to be the centerpiece of your campaign (this week)? Sinking money into a loosing cause, time and time again, with little to no results. Yeah, great. And do I send my tax dollars straight to your personal account Mr. Romney, or do they still go through the IRS before you squander them? If you want to know how he'll handle the nation's budget, just look at how he handles his own money.

Now its one thing to do 'dumb with money'. Its one thing to tour the country, frivolously spending money. Its quite another to lie about it and try to hide it. Poor Mitt got a tad testy with Tim Russert during the Florida debate when the NBC Washington Bureau Chief asked him point blank how much from his personal fortune had he spent on his own campaign. Squirming doesn't begin to cover it. He stuttered, he dodged, he even tried to hide behind the excuse of not wanting to disclose those numbers to his opponents before he had to. Oh, Mitt.... they already know that you are outspending them, they just want to know how hard they should be laughing.

What we already know...

Mitt out-spent Mike Huckabee 15 to 1 in Iowa. Mitt dropped $1 million on advertising with the De Moines AM station, WHO. That put him between Monsanto and Bayer in terns of ad money spent with WHO in 2007. Monsanto and Bayer were advertising fertilizer. Mitt was spreading some too. Huckabee took Iowa.

What to do? More money?

Mitt out-spent the John McCain 3-1 in New Hampshire, dropping $3.6 million on 3600 ads on WMUR (New Hampshire's only state-wide network). McCain took NH.

More recently, Romney's philosophy of spend-more-money failed to buy him the state of Florida.It's also raging in paid advertising on TV and radio. Romney has spent $30 million on TV ads in Florida this year. That's five times as much as the McCain campaign, which is now using less-expensive radio commercials to directly question Romney's credibility on the economy.

So how's that working out for you, Mitt?

1/28/2008

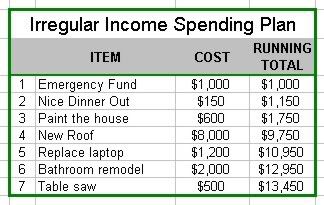

How To: Handle Irregular Income

I've mentioned this a couple of times before - and considering the age of this site, that's really saying something. What to do with irregular income? Even if you are not living on a monthly budget - and you should be - you can still do this. Overtime pay, a bonus check, garage sale profits, inheritance money, tax refund, birthday money... This money is coming in, but what will you do with it?

As you may have found already, if you don't tell your money what to do, you'll always wonder what happened to it. You'll have blown through this extra income so fast, your head will spin and just when you regain your balance, your spouse will say, "Why don't we take that tax refund and do X?". I don't know what 'X' will be, but it won't be a fun conversation when the two of you realize that money is long gone.

Much like a budget, an irregular income spending plan (IISP) is a shared set of goals. If we had extra money, what would we do first? What would we do second? If we still had money left over, what would we do next? A simple spreadsheet will do nicely. What you are making is a prioritized list of expenditures with the cost and running total. I might look like this:

It need not be any more complicated than that, but you can add as much detail as you need. Four important things to note:

- You should have some needs and some wants. Enjoy your money, but be sure your priorities are in order.

- You and your spouse need to agree on the priorities. You may think that buying a table saw should be job 1, but since you haven't taken your wife out to a nice meal in 6 months, she may think otherwise.

- You should always have more items in the hopper than irregular income can cover. Who has ~$13k in irregular income?!? You might! You might not. If you do, then you should have a plan for it. If not, then you can move the remaining items up and work on new ones to fill the hopper. Worst case: a rich relative dies and leaves you more money than you could have imagined and it totally blows away your IISP. This is a good problem to have.

- You'll notice my use of the pronoun "we", and mention discussions with your spouse. This is more important for married couples than you could ever imagine, and probably warrants its own article. If you are not on the same page as your spouse, what a peace offering this could be. Sit down with your husband or wife and talk to them about doing this. Talk about how important this is to you and about how you want to do it together - and mean it.

Anyone else have experience doing this? We've done it for 2 or 3 years now and find it works quite well.

**UPDATE** Welcome CoPF readers! If you are new to Not the Jet Set, the please check out our latest posts as well as a bit about this site. Thanks for reading! --- Continue Reading This Post ---

Welcome Carnival of Personal Finance Readers

My HDTV Challenge article is featured in the Carnival of Personal Finance #137! Big thanks to The Dividend Guy for hosting. Looks like I need to write a better description next time I submit an article. A few articles I enjoyed:

- Jason from The Amatureist Financial Journey has a great piece about crappy insurance. It reminds me about the crap state of health insurance in this country and something interesting I found out about my own.

- Laura's article from Green Panda Treehouse on separate finances in a marriage just leaves me asking, "Why?". As someone with shared finances it just seems terribly complicated, but at least they found something that works for them.

- Bob McDonald from The Platinum Years Network asks What if We SAVED Our “Stimulus Package” Checks? What? We should't go out and blow the money like its two weeks after April 15th? Crazy, Bob, crazy (I happen to agree).

1/27/2008

Disclosure Statement

We are not lawyers. We are not certified. We are not the jet set. We are everyday folks, likely not much different from you. Our content is for informational and entertainment purposes only.

This is a personal blog about money and life - specifically our life. Our content represents our own personal ideas and opinions. Any resemblance to professional advice is coincidental. Educate yourself and/or discuss personal finance ideas with a certified financial planner before making important financial decisions.

This policy is valid from 15 March 2009

This blog is a collaborative blog written by a group of individuals. For advertising rates and statistics or questions about this blog, please contact us at jetsetnotthe [at] gmail [dot] com.

This blog does not accept paid topic insertions. However, we will and do accept and keep free products, services, travel, event tickets, and other forms of compensation from companies and organizations.

This blog will be happy to consider your product for review. In order to have your product reviewed on this blog you must provide one product for the blog owner to review and a second like item to use in a giveaway to promote the review. Products that do not fit with the content of this blog will not be reviewed. This blog does not charge a fee for product giveaways.

The compensation received will never influence the content, topics or posts made in this blog. All advertisements will be identified as paid advertisements.

The owner of this blog is not compensated with cash to provide opinion on products, services, websites and various other topics. The views and opinions expressed on this blog are purely the blog owners. If we claim or appear to be experts on a certain topic or product or service area, we will only endorse products or services that we believe, based on our expertise, are worthy of such endorsement. Any product claim, statistic, quote or other representation about a product or service should be verified with the manufacturer or provider.

This blog does not contain any content which might present a conflict of interest.

This work is licensed under a

Creative Commons Attribution-Noncommercial-No Derivative Works 3.0 United States License.Some rights reserved. Any of these conditions can be waived if you get permission from the copyright holder. Please contact us at jetsetnotthe [at] gmail.com to inquire. Thanks. --- Continue Reading This Post ---

1/26/2008

Free Money!

At the urging of the Federal Reserve Board Chairman and others, the Bush Administration has pushed an "economic stimulus" plan to avoid a supposed recession. From the outset, I was very curious as to how exactly you do something like that. The answer, apparently, is free money. If you qualify - and something like 116 million Americans do - you'll possibly be getting a tax rebate check in the mail. This may come as early as May or June. $600 for individuals, $1200 for couples (filing jointly) + $300 per dependent child. Congress seems to be following along with this plan, though we know how that goes.

This proposed plan, including all of the other rebates that would benefit businesses, is purported to cost the government somewhere in the neighborhood of $150 billion. Its well known that our federal government is not operating in the black. So our nation goes deeper into debt to stimulate our nation's economy? Republican Presidential Candidate Mike Huckabee is skeptical of the whole thing, and I think he's right. Our government will likely borrow the money from a foreign country to give it to Americans, who will likely blow it on products made in foreign countries. So who's economy are we stimulating?

I'll add that if you aren't already living on a budget, if you don't have a spending plan for your money, then you can kiss this money goodbye. You'll have it spent faster than you can say, "Who ran up the Visa bill?". You won't use it to pay down debt (which you should). You won't save it for a rainy day (at least not for more than a couple months). A year from now, you won't even be able to point to something and say, "That's what we did with it, that's how it help our family". If you're not already, then it's time to get on a real plan. Its time to get out of the clutches of debt. This free money from the government may be just the thing to get your debt snowball started.

Full Disclosure: If this check from Uncle Sam comes in ( big IF), ours will got straight into our savings till we apply it to our Irregular Income Spending Plan.

***Update 2/15/2008 *** The checks ARE coming. Does this change our position? No. Read what Dave Ramsey has to say about the 'stimulus package' here.

1/17/2008

The HDTV Challenge

This idea has been kicked around in our house since we moved in - Get rid of the old tube TV (its not that old) and hang a flat-panel TV on the wall. Right now, we have the TV in an entertainment center as well as a mid-century stereo cabinet in the living room. Now, we 'inherited' the stereo, but we love it. Its in great shape, though the turn table won't turn. Right now, its kind of a waste of space. So what if we used that as an entertainment center? With a flat-panel hanging above it? This would free up so much space for us, and look really cool. Now here's the kicker - my wife is the one pushing for this.

As you can imagine, I'm on board. But as you'll see on this blog, we live on a budget, we don't buy things we can't afford, and we don't use credit cards. Since the inception of this grand scheme, it has seemed like a far off dream with no real plan to get there. That is until the other day when my wife asked about what we would do with the "old" TV. Thats when it hit. Sell it. Could we make this happen simply by selling things we already had, but didn't need? What if the answer to getting something new meant purging old things? What if to get ahead, we sacrificed instead of splurging? Crazy.

So based on some quick research into models that would meet our needs (ok, and a few wants), this is going to be a $1000 to $1500 transaction, easily. Mind you, we have some stuff to sell. Not a lot of stuff, but we're coming up with more than we anticipated. So far we have a list of items for sale totaling just under $1400. I know that seems like a lot, but keep in mind that those numbers include our current TV and entertainment center. Needless to say, we are going to sell as much of the other stuff as we can before putting those two on the market.

The original goal was to get this done by Christmas, as we were starting just after Thanksgiving. That didn't go so well, but we got a good start. The secondary market in this area, while it does exist, is a tad slow. Christmas came and went. To date we have banked ~$400 in our challenge. A respectable figure, though well short of the goal. We have sold several items and feel great about them leaving our property in exchange for some much more useful cash. We'll continue the challenge but, with a more open-ended time frame. They're still making TVs, and we're in no rush. A little more time for research wouldn't hurt either. Patience is key. Tom Petty knew what he was talking about when he said that the waiting is the hardest part. We still really like the idea that to get this item (definitely a 'want') we must sell things we have. We are a bit amazed by the amount of stuff we are coming up with to sell. $400 in a month and a half, just by selling a few items, and without trying that hard. May make you think differently about some of the junk you have lying around the house and what you could turn it into.

So how are we doing this? As I said, we don't have a lot of extra stuff to sell. Some years back we started on the Dave Ramsey plan. If you are unfamiliar, he heavily encourages garage sales and ebay to purge the crap you don't need. Wouldn't you rather have the money to pay off the debt you accrued while accumulating the clutter? Well, we sold our crap, and paid off our debt. In fact, we were pretty lean. After relocating last year, the situation changed. Certain things we didn't need anymore or wouldn't fit our decor, or just wouldn't fit period. And this house didn't exactly come empty. So far, we have used Craigslist and my employer's want ads to sell items. Also, my wife has sold quite a few of her crafts (she's a great seamstress and her wares are supercool). Thats really been it. We have some items that will make their way to ebay shortly. Also, we were given some money for Christmas, but that will be going into the Irregular Income Spending Plan. We are adamant to stick to our plan and not take the easy way out.

So how are we doing this? As I said, we don't have a lot of extra stuff to sell. Some years back we started on the Dave Ramsey plan. If you are unfamiliar, he heavily encourages garage sales and ebay to purge the crap you don't need. Wouldn't you rather have the money to pay off the debt you accrued while accumulating the clutter? Well, we sold our crap, and paid off our debt. In fact, we were pretty lean. After relocating last year, the situation changed. Certain things we didn't need anymore or wouldn't fit our decor, or just wouldn't fit period. And this house didn't exactly come empty. So far, we have used Craigslist and my employer's want ads to sell items. Also, my wife has sold quite a few of her crafts (she's a great seamstress and her wares are supercool). Thats really been it. We have some items that will make their way to ebay shortly. Also, we were given some money for Christmas, but that will be going into the Irregular Income Spending Plan. We are adamant to stick to our plan and not take the easy way out.

So what's it really worth?: Curtain Rods

What is a $45 curtain rod really worth? I don't know, but I just bought one for $2.

What is a $45 curtain rod really worth? I don't know, but I just bought one for $2.Whaaa? Ok, so the finial on one end was damaged, though it's pretty hard to tell. It had been placed on the clearance cart (one of our favorite hang-outs) as we were walking by - while shopping for curtain rods. It was the size we needed, the style would work for the room, and the price was beyond right. They even had the piece that was broken off of the cast finial with the rest of it. With the sharpie ink still drying on the label, we carried off our find.

The rod is now installed and looks great. The $43 part that was broken off of the finial is sitting on the end table. Not sure what we'll do with it.

"So what's it really worth?"

Opposites do attract, but something my wife and I both thoroughly enjoy is getting deals. We're pretty good at it, too. But we get it honestly - both sets of our parents know how to get a deal and do so regularly. My father, for example, was showing me a couple of beautiful suits he'd purchased recently. Both brand name, purchased at retail at a savings of several hundred dollars. Then came the phrase, "So what's it really worth?". A question of his that I rarely have the answer for.

I typically - true or not - assume a 100% mark-up at retail. That means if the store's cost-of-goods-sold is $100, then they'll be pricing it at $200 (ok, ok, $199.95). Sure some items are loss-leaders - meaning the store takes a hit on the item to get you in the door and buy other items as well. Some items may be ringing up at more like 1000% mark-up. Thats right, an order of magnitude. Try pricing out some AV cables at Best Buy, and then see what you can get them for on-line, you'll see what I mean. At any rate, they're marking it up to cover overhead and turn a profit, thus they can afford to later knock it down "on sale".

The pricing games played at retail are terrible these days - pricing items well above MSRP just to discount it immediately so that you feel good about saving 50%! Not all retailers are guilty of that example, but it seems to be plaguing places like Kohl's and Sears. Some deals are just that - deals. Some are not. How retailers think they can pull this off in the information age is beyond me.

So what's it really worth? How much is a $500 suit really worth? $70 for an HDMI cable? I don't always have the answer to these questions, but I can tell you this: Its generally not worth what they are asking for it. This reoccurring space will be dedicated to those times when we truly, honestly get a deal and have to ask, "So what's it really worth?".

Welcome

After playing around with this site for a while, I think I've gotten to a point where I might, kinda get serious about blogging. I know, way to commit! I feel I have a lot to say about personal finance, it's just a matter of making the time to make something out of this. A few things to note:

- I did not major or minor in English. Feel free to correct my grammar or spelling, just don't expect me to care. On second thought, don't bother.

- I am not a financial planner, financial counselor, nor accredited in any way in this field. I am, however, an expert in my opinion.

- I welcome intelligent discussion or debate about the topics of my posts, but I will moderate comments and reserve the right to remove inappropriate comments.

- I am a fan of Dave Ramsey and my opinions tend to line up with what he teaches.

- I think Suze Orman is a shill.

- I will mostly be blogging about personal finance as it relates to current events, faith, and everyday life.

- I am not doing this for money,

and you will not see ads on this blog.See here for more on this. - I am not independently wealthy, and have earned all that we have.

- I am not afraid to fail and have done so before.

- I have a wife, 2 children, a mortgage, and no other debt (thanks, Dave!).

- I am hopelessly frugal, but by no means a scrooge. I enjoy life, but not at the expense of my family's future.

If you have questions, ASK! I'm happy to discuss.

--- Continue Reading This Post ---

1/01/2008

About Us

He's a spender, she's a saver. Together, they're Not the Jet Set.

Fed up with working too hard to not have any money, we made the decision to take control of our finances. We began a mission to get out of debt and stay out of debt - forever. On June 23rd of 2006, we completed Baby Step 2 by paying off over $42,000 in 20 months. During that time and ever since then, we've seen it as part of our calling to help others achieve what we have - financial peace.

not the jet set . net is a blog about money, stewardship, and frugal living - personal finance for the rest of us: one family's story. We don't claim to know it all. We won't claim to make you rich. But we may get you to think a little differently about money and how it affects your life.

Be sure to check these out if you haven't already.

- Who is Mrs. Not the Jet Set?

- We're (Still) Debt-Free!

- Our Cash Envelope System

- The Reluctant Spouse

- Our Budgets

- 2008 Year in Review

Contact Info

Wanna chat? Got a question? Drop us a line!

Want to advertise on Not the Jet Set? Interested in product reviews or giveaways? Drop us a line and we can discuss details.

--- Continue Reading This Post ---

Subscribe to:

Posts (Atom)

{kind=link}

{kind=link}